By Amber Liu, China Briefing, Dezan Shira & Associates

Reading time: 6 minutes

Following the announcements made in the annual Work Report delivered at the Two Sessions, the Ministry of Finance, State Taxation Administration, and General Administration of Customs have jointly issued a series of new policies on value-added tax (VAT).

The new polices, which took effect on April 1, 2019, aim to enhance economic activity in certain sectors by lowering VAT rates and increasing VAT credits.

The latest changes mark the final stages of China’s overhaul of its VAT system, and come as part of a larger RMB 2 trillion (US$298.3 billion) cost cutting package intended to boost China’s economy

Here, we highlight five major changes to the new VAT policies.

1. Reducing VAT rates

Beginning April 1, 2019, taxpayers who were originally subject to VAT rates of 16 percent and 10 percent imports or exports of goods and services, will now be subject to an adjusted 13 percent and 9 percent, respectively.

The 10 percent deduction rate on agricultural products purchased by taxpayers will be adjusted to 9 percent. For agricultural products purchased by taxpayers for production or commissioned processing, the input VAT will be calculated at a 10 percent deduction rate; previously, it was subject to VAT at 13 percent.

Moreover, for goods purchased by overseas visitors, the departure tax refund rate has now been adjusted to 11 percent and 8 percent from 13 percent and 9 percent, respectively.

Transitional rules

The tax position during the changeover period has been further clarified to ensure a smooth transition into the new VAT rates. Generally, if the VAT invoice was generated or issued prior to April 1, 2019, the old tax rate will apply – this point is illustrated and expanded upon in the examples below.

Example 1: If a VAT invoice has been issued prior to April 1, 2019, any corresponding negative VAT invoice issued – due to sales discount, sales return, sales cancellation, or inaccuracies in the original VAT invoice – will also be subject to the old tax rate.

Example 2: In situations where a general VAT taxpayer has not issued VAT invoices for taxable income generated before April 1, 2019 but needs to issue such invoices on or after April 1, 2019 – the VAT invoicing will be done at the old tax rate.

2. Changing the redemption of input VAT credit for real estate and projects under construction

From April 1, 2019, a business registered as a general VAT taxpayer can claim the full input VAT credit all at once for purchases of real estate and construction services.

Previously, the old rule stipulated that the input VAT credits for purchases of real estate and construction services are claimed over a two-year period.

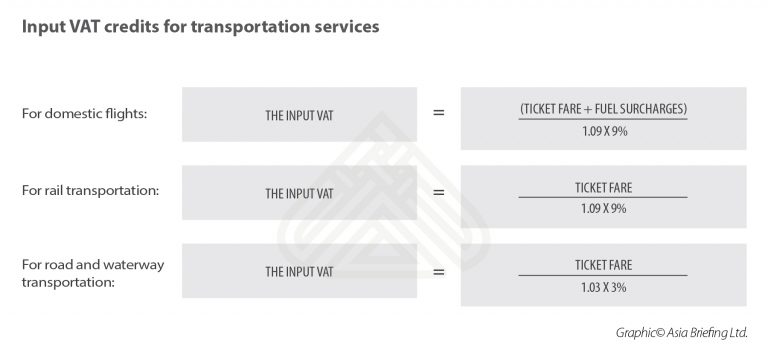

3. Allowing input VAT credits for transportation services

Businesses registered as general VAT taxpayers can now claim input VAT credits for domestic passenger transport services and credit its input tax against its output tax.

However, the input VAT for transportation services will be calculated differently according to the documentation provided and mode of transportation taken.

For taxpayers who fail to obtain a special VAT invoice, but can obtain an electronic general VAT invoice, the input VAT credit is the amount indicated on the electronic general invoice.

Alternately, for taxpayers who can claim input VAT credits for domestic flights, rail, road, and waterway transportation services using supporting invoice or ticketing documentation and passenger ID information, the following formulas apply.

4. Allowing VAT additional deductions for certain industries

During the period between April 1, 2019 to December 31, 2021, taxpayers in the following service industries are eligible for a 10 percent additional VAT deduction based on deductible input VAT in the current period:

- Postal and telecommunications services;

- Research and development, technical services, information technology services;

- Cultural, sports and creative services;

- Logistics and ancillary services;

- Certification, consulting, and business support services;

- Accommodation and leasing services;

- Education and healthcare; and

- Travel and entertainment services.

Taxpayers shall set up separate accounts to track the movement of the additional deduction and its balance.

5. Allowing VAT refund for excess input VAT credits

In the past, when a company’s input VAT exceeds the output VAT, the excess VAT credits can be carried forward to offset the output VAT incurred in the next tax period.

Under the new policy, businesses are able to enjoy a refund on their excess input VAT (meaning added cash flow for the company), if they are able to meet the following criteria:

- If the incremental overpaid VAT for each of the six consecutive months (two consecutive quarters if taxed quarterly) is a positive number, and the incremental overpaid VAT in the sixth month is not less than RMB 500,000 (US$74,561);

- The taxation credit is rated as A or B;

- There has been no VAT fraud in the last 36 months prior to claim;

- There have been no penalties by tax authorities 36 months before its claim for VAT refund; and

- They have not received refunds on their levy.

Preparing for the new changes

To prepare for these reforms, businesses are advised to reflect on how the new changes affect both their internal management systems and external business operations.

In doing so, businesses should carefully review their agreements and processes to ensure this is in line with the new VAT policies.

This includes reviewing the purchase and sales contract with suppliers and customers as well as internal software – such as their VAT invoicing andERP system.

With regards to the ERP system, businesses should review the VAT rates under the purchase and sales modules, inform key users of such changes, and perform regular checks to make sure the rates are chosen correctly.

Enterprises are also advised to check whether they are eligible for the 10 percent additional VAT deduction as well as the refund for excess input VAT credits.

Finally, enterprises are advised to share the new policy of input VAT credits for transportation services with staff to make sure they get proper support for their travel.

If the company has an established ERP system, it is necessary to update the system to allow their staff to fill in input VAT amount (or calculate the input VAT automatically by the system) when the travel expenses reimbursement applications are filled in the system.

For travel expenses – enterprises are also advised to differentiate business-related travel from travel carried out for staff welfare purposes as the latter is not allowed for input VAT deduction.

About the Author

Amber Liu

Amber Liu is senior manager of accounting and tax services team in South China, located in Dezan Shira & Associates’ Shenzhen office.

She graduated from Southwest University of finance and economics, and is a Chinese Certified Public Accountant (CPA).

Amber worked for 2 years in a multinational manufacturing company and 2 years in a real estate company, and has more than 9 years of Chinese accounting and tax consulting experience.

Amber specializes in accounting and reporting, tax planning, internal control and also transfer pricing issues.

Dezan Shira & Associates

Since its establishment in 1992, Dezan Shira & Associates has been guiding foreign clients through Asia’s complex regulatory environment and assisting them with all aspects of legal, accounting, tax, internal control, HR, payroll and audit matters. As a full-service consultancy with operational offices across China., Hong Kong, India and ASEAN, Dezan Shira & Associates is your reliable partner for business expansion in this regional and beyond.

Original article link: https://www.china-briefing.com/news/5-big-changes-chinas-vat-2019/

This article was first published by China Briefing, which is produced by Dezan Shira & Associates. The firm assists foreign investors throughout Asia and maintains offices in China, Hong Kong, Indonesia, Singapore, Russia, and Vietnam. Please contact info@dezshira.com or visit our website at www.dezshira.com.